Picture Sarah, a cheery barista in Brighton, earning a decent £35,000. Yet, payday brings more pressure than relief. The rent swallows a chunk, groceries deplete the rest, and dreams of Brighton Pier seem distant. Sarah isn’t alone. Figuring out your “35,000 after tax” reality is crucial in the UK, and this guide aims to be your financial compass.

Understanding Your Take-Home Pay:

The Tax Maze: Taxes, eh? Don’t let HMRC’s demands leave you bewildered. Let’s untangle the knot:

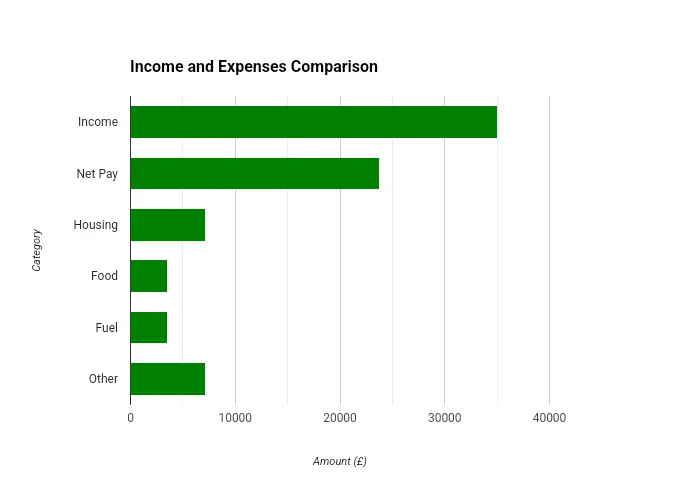

- Income Tax: Your 35 grand falls into a 20% tax bracket, leaving you with a cool £28,000. But hold on, that’s just the start! National Insurance contributions (NICs) at 12% chew off another £4,200.

- Regional Variations: Scotland has its own income tax bands, so your net pay might differ slightly north of the border.

Deductions and Credits: Claim back your hard-earned cash!

- Pensions: Contributing to a workplace pension scheme grabs you tax relief, giving your retirement nest egg a boost.

- Student Loans: Repaying student loans qualifies you for tax relief, easing the burden a tad.

Employer Withholdings: Pay slips can be daunting. We’ll break them down:

- Pay Before Tax (PBT): Your gross salary before the taxman takes his share.

- Deductions: NICs, student loan repayments, pension contributions.

- Net Pay: What finally lands in your bank account.

Calculating 35k After Tax: Unveiling the Net Pay Maze

Taking home £35,000 sounds manageable, but just like navigating a labyrinth, finding your exact net pay involves twists and turns of tax deductions and allowances. Worry not, intrepid explorer, for we’ll compare online tools to demystify your post-tax income:

| Tool | Take-Home Pay (Annual) | Monthly Pay | Weekly Pay |

|---|---|---|---|

| Reed.co.uk | £27,186 | £2,265 | £523 |

| Vatulator.co.uk | £27,305 | £2,275 | £527 |

| SalaryCalculators.org | £27,822.40 | £2,318.53 | £535.05 |

| UKTaxCalculators.co.uk | £27,944 | £2,328.67 | £539.67 |

| Income-Tax.co.uk | £27,822 | £2,318.53 | £535.05 |

As you can see, the net pay for £35,000 ranges from £27,186 to £27,944, a difference of almost £800! This variation stems from how each tool accounts for factors like:

- Personal Allowances: Depending on your circumstances, you may be entitled to tax-free allowances that reduce your taxable income.

- National Insurance Contributions (NICs): These mandatory contributions fund public services and are deducted directly from your salary.

- Employment Status: Full-time, part-time, and self-employed individuals have different tax implications.

- Student Loan Repayments: If you have outstanding student loans, repayments are typically deducted before you receive your pay.

Budgeting with 35,000 After Tax:

| Topic | Key Points |

|---|---|

| Take-Home Pay | – Income tax: 20%, leaving £28,000 – National Insurance contributions (NICs): 12%, reducing pay to £23,800 – Regional variations (Scotland) |

| Deductions & Credits | – Pensions: tax relief for contributions – Student loans: tax relief for repayments |

| Employer Withholdings | – Pay Before Tax (PBT) – Deductions: NICs, student loans, pension – Net Pay: final amount in bank account |

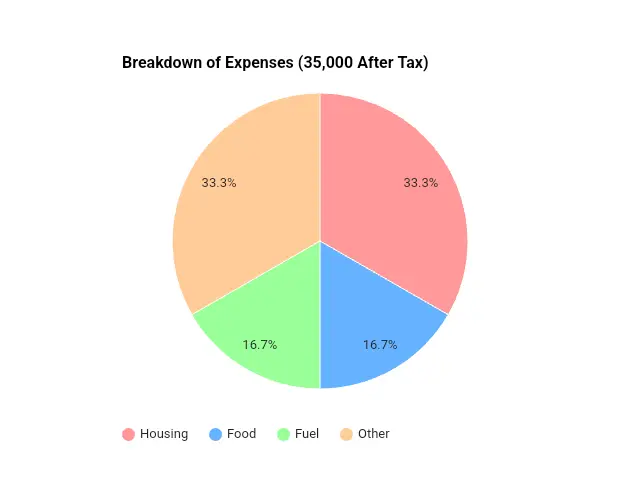

| Budgeting | – 30% housing: £700 for Sarah in Brighton – 10-15% food: £350-£450 for Sarah – 10-15% fuel & transport: £350-£450 for Sarah – 20-30% other expenses |

| Debt Management | – Prioritize high-interest debts: snowball or avalanche methods – Negotiate and consolidate loans |

| Savings & Investments | – Emergency fund: 3-6 months’ living expenses – Retirement: workplace pension, ISA contributions |

| Lifestyle Tweaks | – Groceries: meal planning, store brands, cooking at home – Dining out: pack lunches, limit takeaways – Transport: cycle, walk, public transport, carpool |

| Boosting Income | – Side hustles: freelancing, online gigs, tutoring, etc. – Upskilling and promotion |

| Advanced Strategies | – Tax optimization: deductions, credits, ISAs – Building wealth: stocks, ETFs, mutual funds, diversification |

Living Wisely: Making £23,800 (after NICs) stretch requires smart budgeting. Here’s a rough breakdown:

- Housing: Around 30%, so for Sarah in Brighton, rent might be roughly £700. Check the average costs in your area using resources like Shelter.

- Food: Aim for 10-15%, around £350-£450 for Sarah. Meal planning, budget supermarkets, and home cooking can be your knight in shining armour.

- Fuel and Transport: 10-15%, around £350-£450. Consider cycling, walking, or public transport where possible.

- Other Expenses: 20-30%, covering everything from bills to leisure. Use free activities in your town, like museums or parks, to make the most of your leisure budget.

Download our budgeting template to customize your spending plan!

Debt Management: Oweing money? Tackle it head-on:

- Prioritize High-Interest Debts: Credit card debt? Use the snowball method (paying off smaller debts first) or the avalanche method (targeting debts with the highest interest rates).

- Negotiate and Consolidate: Don’t be afraid to haggle for lower interest rates or consider debt consolidation loans to simplify your repayments.

Savings and Investments: Every penny counts!

- Emergency Fund: Aim for 3-6 months’ worth of living expenses to weather unexpected storms.

- Retirement: Starting a workplace pension is crucial. Consider ISA contributions for additional long-term savings.

Check out – VAT Calculator

Lifestyle Tweaks for a Fatter Wallet:

Cost-Cutting Champions: Small changes, big impact:

- Groceries: Plan meals, compare prices, embrace store brands, and cook at home.

- Dining Out: Pack lunches, limit takeaways, and enjoy free entertainment like picnics in the park.

- Transport: Cycle, walk, use public transport passes, or carpool.

Boosting Your Income: Want a little extra? Explore these options:

- Side Hustles: Freelancing, online gigs, tutoring, pet-sitting – unleash your skills for extra cash.

- Upskilling and Promotion: Invest in new skills to climb the career ladder and boost your salary.

Advanced Strategies for Financial Fitness:

Tax Optimization: Legally minimize your tax bill:

- Claim all eligible deductions and credits.

- Utilize tax-efficient savings like ISAs.

Building Wealth: Secure your future:

- Invest in stocks, ETFs, or mutual funds.

- Diversify your portfolio to manage risk.

- Seek professional financial advice if needed.

Sarah’s Success Story:

Follow Sarah as she implements these strategies. Watch her optimize taxes, navigate budgeting, and land a lucrative side hustle as a photographer. Her journey proves that financial security on £35,000 is achievable!

Conclusion:

Living comfortably on £35,000 after tax isn’t a walk in Hyde Park, but it’s far from an impassable Everest. Remember, Sarah, our Brighton barista, navigated the maze, and so can you! Now, let’s wrap up with some final takeaways:

Key Points to Remember:

- Understand your take-home pay: Taxes and deductions nibble at your salary, but knowing the numbers empowers you to budget effectively.

- Budgeting is your best friend: Allocate your income smartly, prioritizing essentials and finding room for fun without breaking the bank.

- Embrace smart living: Cost-cutting hacks and alternative transportation can stretch your pounds further.

- Explore income boosts: Side hustles and career advancement can add valuable financial fuel.

- Plan for the future: Saving for rainy days and building long-term wealth are crucial for future peace of mind.

Take Action and Thrive:

- Download our resources: Use the budgeting template, tax checklist, and other downloadable tools to personalize your financial journey.

- Stay informed: Subscribe to our newsletter for updates on tax laws, cost-of-living changes, and financial tips.

- Seek support: Don’t hesitate to reach out to financial advisors, debt management counselors, or even online communities for guidance.